Fundrise vs Yieldstreet [2025] Yieldstreet vs Fundrise

By Maddy Scheckel

By Maddy Scheckel The Money Manual earns a commission for this endorsement of Fundrise.

When you hear “invest,” you might think of the stock market.

That’s no surprise. 61% of American adults reportedly own stock – so it’s “top of mind” for a lot of people.

But to limit risk and improve your yields, it’s often best to “diversify” your portfolio by investing in alternative assets, like real estate. It sounds tricky, I know – but it’s easier than ever, thanks to platforms like Fundrise and Yieldstreet.

Below, I’ll walk you through a detailed Fundrise vs Yieldstreet comparison – discussing fees and returns along the way.

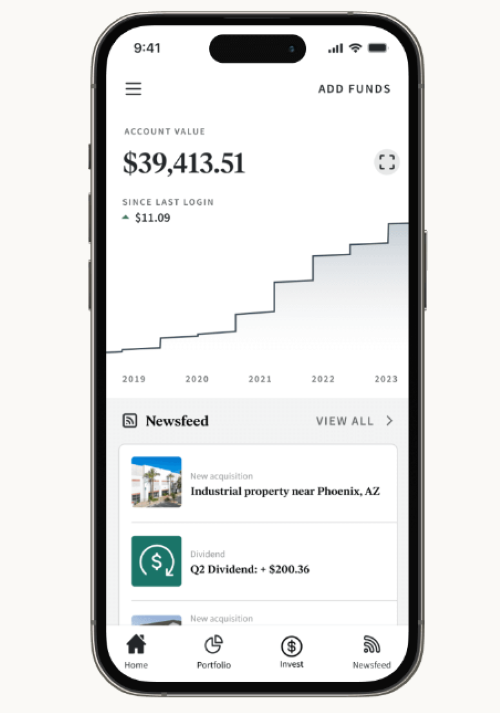

While most of us can’t afford to buy rental properties outright, you can start buying partial shares in real estate through a platform called Fundrise.

You can get regular updates on your investments through your account, including milestones like new construction progress, occupancy reports, market data trends, and project completion alerts.

If you want to dip your toe into real estate investing, Fundrise is one of the best ways to do it.

Fundrise vs Yieldstreet Overview

It’s obvious why the Fundrise vs Yieldstreet comparison is an important one to make. These are two of the most well-known alternative investment platforms.

But are they exactly the same? No.

One focuses primarily on real estate and lets you invest as little as $10. That’s Fundrise.

The other offers alternative assets like artwork and has a $10,000 minimum. That’s Yieldstreet.

See? These platforms are more like distant cousins than identical twins!

Next, I’ll dig deeper into the Fundrise vs Yieldstreet discussion by summarizing how each one works.

If you want to start investing but aren’t sure where to begin, check out our guide to investing for beginners.

What is Fundrise and How Does Fundrise Work?

Fundrise is a real estate investment platform that lets you get started with as little as $10. It’s well known for its real estate investment funds, but it also offers investments in private credit and venture capital.

The basic premise of Fundrise is simple: They pool investors’ money to buy and manage a portfolio of properties. As an investor, you get a share of the returns when the portfolio makes money.

The Fundrise portfolio is big. Just how big? It consists of 290 active projects worth more than $7 billion in total. And those investments have attracted over 2 million users.

Source: Fundrise

Here’s how to invest in real estate through Fundrise:

- Create a Fundrise account online. You don’t have to be an accredited investor, and the minimum investment is just $10, making Fundrise accessible to almost anyone. You can choose to open an Individual Brokerage Account or an Individual Retirement Account (IRA).

- Invest! You can buy into the Fundrise portfolio or make alternative investments in private credit or venture capital.

- Collect your returns. If your investments make money, you can withdraw your earnings on a quarterly basis.

Want to take a more active role in your Fundrise investments? For $10 a month, a Fundrise Pro membership gives you full control of your investment portfolio. You’ll be able to create custom investment plans and invest directly into all available funds on the platform, including limited-access, strategy-specific funds.

Just remember that Fundrise is an “illiquid” investment. The initial money you’ve invested in real estate will remain out of reach for 5 years. You can always request an early liquidation to access your money earlier, but you’ll probably have to pay a penalty (1% of total share value).

*Note: Yieldstreet’s investments are also “illiquid,” so this isn’t a point for either team in the Yieldstreet vs Fundrise debate.

Want to learn even more about how Fundrise works? Read this complete Fundrise review.

What is Yieldstreet and How Does Yieldstreet Work?

Yieldstreet is a crowdfunding investment platform that focuses on real estate and “alternative investments.”

You can use Yieldstreet to invest in multiple asset classes, including:

- Real estate

- Art

- Private Equity

- Transportation

- Crypto

- Venture capital

- Private credit

- Short-term notes

- Legal

In the world of investment platforms, Yieldstreet is truly a “Jack of all trades.”

When it comes to size, Yieldstreet loses the Fundrise vs Yieldstreet battle – but not by much. Yieldstreet has more than 450,000 members, and those users have invested over $3.9 billion in the platform. Over the years, those investors have earned more than $2.4 billion in returns.

Source: Yieldstreet

Want to get a piece of the action? Well, here’s some good news: Yieldstreet is super easy to use. In fact, when it comes to convenience, the Yieldstreet vs Fundrise competition is pretty much a tie. They’re both user-friendly, and neither requires members to be “accredited investors.”

The main limitation with Yieldstreet is the minimum investment of $10,000. That puts the platform out of reach for many investors.

For those of you who can afford the minimum investment, here is the 3-step process for using Yieldstreet:

- Browse the selection of investment opportunities. Yieldstreet offers three broad categories of investments: Some that prioritize current income, some that prioritize future growth, and others that strike a balance between the two.

- Invest in your chosen assets. All the investments on the platform pass through a 4-step vetting process. You’ll also have access to vital financial details, allowing you to make informed decisions.

- Track the performance of your portfolio. Yieldstreet keeps you up to date on how your investments are doing.

Are you interested in alternative investments? Yieldstreet is a great option – but it’s not your only option. Check out this article for more ideas on alternative investments.

If you’re interested in learning more about precious metals as an alternative investment opportunity, check out our Goldco vs Augusta Precious Metals comparison.

And if you’re interested in learning more about wine and spirits as an alternative investment, our Vint vs Vinovest comparison can help.

Fundrise vs Yieldstreet Fees

Here’s some bad news that shouldn’t come as a surprise: Fundrise and Yieldstreet both charge fees.

But how much can you expect to pay?

It’s time for this Yieldstreet vs Fundrise analysis to break down the costs.

Fundrise Fees

Fundrise fees are super simple. If you invest in the real estate portfolio, you’ll be responsible for two annual fees:

- An “advisory” fee of 0.15% per year

- A “management” fee of 0.85% per year

So, let’s imagine you invest $1,000 in Fundrise. In a year, you’ll have to pay $1.50 for the advisory fee and $8.50 for the management fee. That’s a total of $10 – which is reasonable, right?

The simplicity of the fee structure is one area where Fundrise wins the Fundrise vs Yieldstreet battle!

Yieldstreet Fees

Yieldstreet’s fees vary depending on the investment.

In general, Yieldstreet members face three types of fees:

- Listing fees. These are flat, one-time fees that are sometimes waived altogether, depending on the investment.

- Management fees. These range from 1 – 4%, charged annually.

- Annual flat expenses. These will depend on the legal structure of the specific investment and are paid from initial interest distributions.

*Note: When you see the “targeted returns” listed for a potential investment, these returns already take the fees into account. So, you don’t have to subtract them yourself from your potential earnings!

It’s tough to be specific when describing Yieldstreet’s fees because there are so many assets offered on the platform, and they all bring different costs.

Let’s focus on the fees for the Yieldstreet Alternative Income Fund. Formerly called the “Yieldstreet Prism Fund,” it’s the platform’s flagship alternative investment opportunity – with assets including real estate, private credit, and even artwork.

Members who invest in the Yieldstreet Alternative Income Fund face two different fees:

- An annual management fee of 1%

- Annual administrative expenses that can reach a maximum of 0.5%

You might not be charged for all the money you’ve placed in the fund. Any money that’s kept in cash (rather than invested) won’t be subject to the fees.

Fundrise vs Yieldstreet Returns

I bet I know what’s most important to you as you consider the Fundrise vs Yieldstreet debate: Which platform will give you the largest returns?

Luckily, both platforms are super transparent about how their investments have fared. I’ll pull out the key data points below.

Fundrise Returns

Over the past 5 years, Fundrise’s real estate portfolio has had an average annual return of 6.7%. That’s pretty solid, right? But remember, that’s just an average. There have been some especially good years (and an especially bad year) during that 5-year stretch.

Here’s a year-by-year breakdown of Fundrise’s average annual returns:

- 2024: 5.75%

- 2023: -7.45%

- 2022: 1.50%

- 2021: 22.99%

- 2020: 7.31%

- 2019: 9.16%

Real estate investments are never risk-free. Even an investment like Fundrise, where experts manage the portfolio, can suffer a major slump (like in 2023). It’s important to keep that inherent risk in mind when thinking about Yieldstreet vs Fundrise. You could lose money on either platform!

But then there’s the upside: Fundrise investors earned 22.99% in 2021! And it had bounced back to a healthy 5.75% by Q4 2024. This is the nature of a longer-term investment.

Yieldstreet Returns

Yieldstreet’s investments over the years have given investors an internal rate of return (IRR) of 9.6%.

Here are Yieldstrest’s average annual returns on different types of assets:

- Legal – 13%

- Art – 10%

- Real estate – 9%

- Transportation – 9%

- Private credit – 9%

- “Other” – 8%

- Short-term notes – 5%

The Yieldstreet Alternative Income Fund, which is the platform’s flagship product, has a net annualized yield of 8.3%.

So, that covers how much you might earn – but how will you actually get your money?

Returns will be sent to your “Yieldstreet Wallet,” a savings account that earns interest and is insured by the Federal Deposit Insurance Corporation (FDIC). From there, you can roll the returns into a new investment – or withdraw them.

You can withdraw funds from your Yieldstreet Wallet up to 6 times per month (it can take up to 5 days to process).

Pros and Cons: Fundrise vs Yieldstreet

Fundrise and Yieldstreet have a lot of exciting features. That’s what makes the Fundrise vs Yieldstreet debate so compelling!

But both platforms have their drawbacks, too. I’ll lay out the pros and the cons of each company below.

Pros and Cons of Fundrise

Fundrise Pros

- The minimum investment is only $10. That makes it super affordable to get started.

- The fees are simple and reasonable. When you invest in real estate on Fundrise, you’ll pay just 1% total each year (because of a 0.85% management fee and a 0.15% advisory fee).

- You don’t have to be an accredited investor to sign up. This is another reason Fundrise is so accessible. (And this is true for Yieldstreet, too!)

Fundrise Cons

- The investment is “illiquid.” Withdrawals are only possible once a quarter, and you could face a fee if you haven’t had the investment for 5 years.

- The range of alternative investments is smaller. You can use Fundrise to invest in real estate, private credit, and venture capital – but not art, short-term notes, or transportation assets.

- The average returns are lower than Yieldstreet. Over the last 5 years, Fundrise’s average returns were solid – but not earth-shattering – at 6.7%.

Pros and Cons of Yieldstreet

Yieldstreet Pros

- It offers a wide variety of alternative assets. You can use Yieldstreet to invest in real estate, private credit, artwork, and other assets – or buy into a fund that combines them.

- The returns are often impressive. Yieldstreet’s average annual returns come out to 9.6%.

- The fees are generally reasonable. If you invest in the Yieldstreet Alternative Income Fund, you’ll pay a maximum of 1.5% in combined fees and administrative costs.

Yieldstreet Cons

- The minimum investment is $10,000. So, if you’re just looking to “try out” alternative investments with a minor financial commitment, you’ll have to use a different platform (like Fundrise).

- The investments are “illiquid.” That means you won’t have guaranteed access to your money (it may take up to 15 months for the option of liquidity).

- Alternative investments (like the ones on Yieldstreet) are inherently risky. While Yieldstreet investors have come out ahead overall, there’s always a risk that your specific investment could lose money.

Fundrise vs Yieldstreet Review

One way to get a handle on the Fundrise vs Yieldstreet conversation is by looking at user reviews on Trustpilot.

Let’s start with Fundrise.

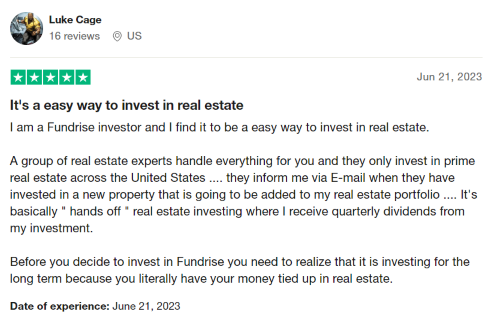

In a 5-star review, someone called Fundrise an “easy way to invest in real estate.”

Source: Trustpilot

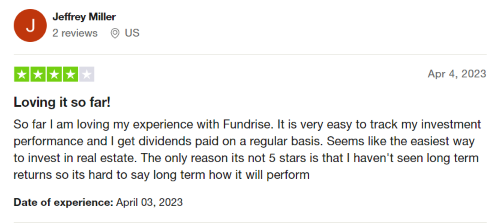

Another user said they were getting “dividends paid on a regular basis,” which is always a good outcome with an investment!

Source: Trustpilot

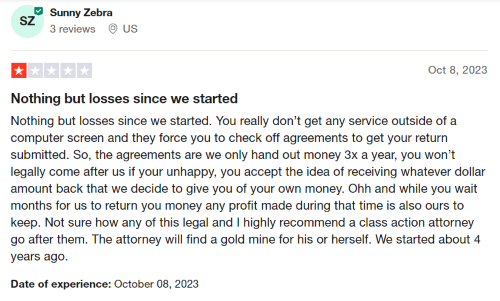

But not all Fundrise reviews are positive. One person said they’d experienced “nothing but losses” since starting on the platform.

Source: Trustpilot

Now, let’s take a look at some Yieldstreet reviews.

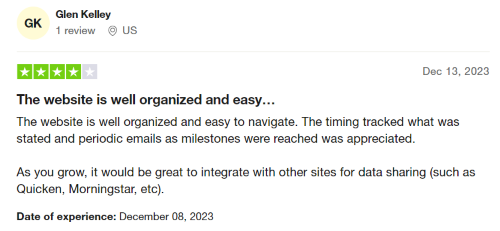

In a 4-star review, a user praised the Yieldstreet website as “well organized and easy to navigate.”

Source: Trustpilot

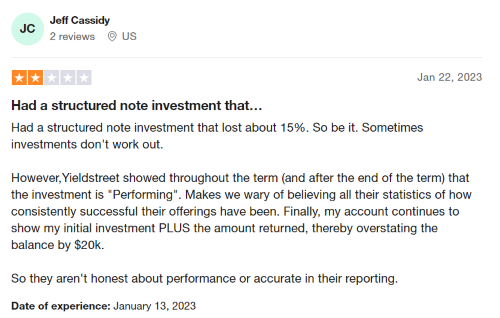

Some other Yieldstreet users expressed frustration with the platform.

In a 2-star review, a user made two complaints: That their structured-note investment lost around 15% and that Yieldstreet wasn’t clear about the performance.

Source: Trustpilot

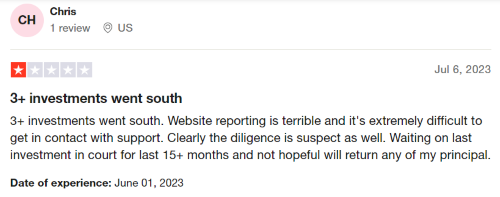

And in a 1-star review, someone said their “investments went south” and that the Yieldstreet website is “terrible.”

Source: Trustpilot

Fundrise vs Yieldstreet Reddit

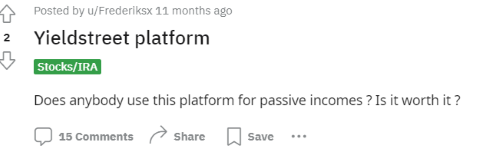

Over on Reddit, I found a threat that relates directly to the Yieldstreet vs Fundrise debate. Someone asked about Yieldstreet, and – surprise, surprise – Fundrise came up in the responses.

Source: Reddit

A few Redditors discussed Fundrise, commenting on the platform’s recent decision to begin investing in venture capital.

Source: Reddit

Another person said they don’t use Yieldstreet themselves but think it could be a great source of passive income.

Source: Reddit

Fundrise vs Yieldstreet: Which is Better?

After comparing all the facts, I’ve decided there’s no absolute winner in the Fundrise vs Yieldstreet battle. Each platform is best for certain types of investors.

Fundrise is better if you:

- Want to invest less than $10,000

- Can afford to part with your money for 5 years

- Want to invest specifically in real estate

Yieldstreet is worth trying if you:

- Can afford to invest $10,000 or more (remember: the bigger the investment, the bigger the possible return!)

- Want to invest in a wide variety of alternative assets

Also, it’s important to remember that there are options outside the Yieldstreet vs Fundrise debate. Before making any actual investments, it’s best to think carefully about your strategy and weigh all your options.

Learn more with this article about the best way to invest money.

Don’t Miss This:

Don’t Miss This:

The Hottest Investing Apps Of 2025: Start Building Wealth Today

Commonly Asked Questions About Fundrise vs Yieldstreet

Is Fundrise Better Than Yieldstreet?

Fundrise is better than Yieldstreet if you want to invest a small amount of money. Fundrise’s minimum investment is just $10, while Yieldstreet has a $10,000 minimum. But in general, there’s no clear winner in the Fundrise vs Yieldstreet debate. Both platforms have made money for investors.

Has Anyone Made Money with Fundrise?

Lots of people have made money with Fundrise. The platform has over 2 million users. And over the past 5 years, Fundrise’s average annual returns have been 6.7%. That means, despite what some negative reviews would have you think, plenty of people have come out ahead.

What is The Fundrise Controversy?

Fundrise suffered a brief scandal in 2016 when a former employee claimed the company had acted illegally – but the claims were never proven. Fundrise says the ex-employee was trying to extort the company.

Yieldstreet vs Crowdstreet?

Both Yieldstreet and Crowdstreet are investing platforms that specialize in crowd-funded investments. Yieldstreet offers a wide variety of alternative investments, while Crowdstreet focuses on real estate. To learn more, read this post on Fundrise vs CrowdStreet.

And if you’d like to learn about how AI can help you manage your portfolio, check out our Streetbeat review.

Fundrise Balanced vs Long Term?

Fundrise’s Long-Term Growth Plan prioritizes future earnings, which should come when assets appreciate in value. The Balanced Investing Plan mixes in some assets that could provide near-term returns in the form of dividends.